Vriti Chheda

The coronavirus pandemic, and its resulting financial shock, is threatening the health of world economies including that of the United States. Fears of an impending global recession continue to rise as governments impose stringent restrictions on businesses in efforts to control the pandemic and as the virus redefines the very notion of public space in the wake of new “social distancing” orders.

On March 13, 2020 the White House declared the coronavirus outbreak a national public health emergency. Consequently, states across the U.S. enforced severe travel restrictions, implemented strict shelter-in-place orders, shuttered non-essential businesses, and banned all public gatherings. These necessary policies, while effective in slowing the spread of the virus, have extremely negative economic implications. As businesses close and states mandate people to stay at home, consumers are left with no opportunities to shop, thus sharply decreasing consumption spending, which is responsible for approximately 70.0% of the U.S. total GDP. This initial drop in spending paired with continued business closures, is forcing businesses to lay off employees in order to reduce costs and minimize losses. As workers get laid off and lose their income, they must reduce their household spending, thus kicking off the multiplier process and further decreasing consumption spending. As consumption spending, the principal engine of the U.S. economy, collapses causing significant contractions in U.S. real GDP and total economic output, Americans face the looming risk of an inevitable economic recession.

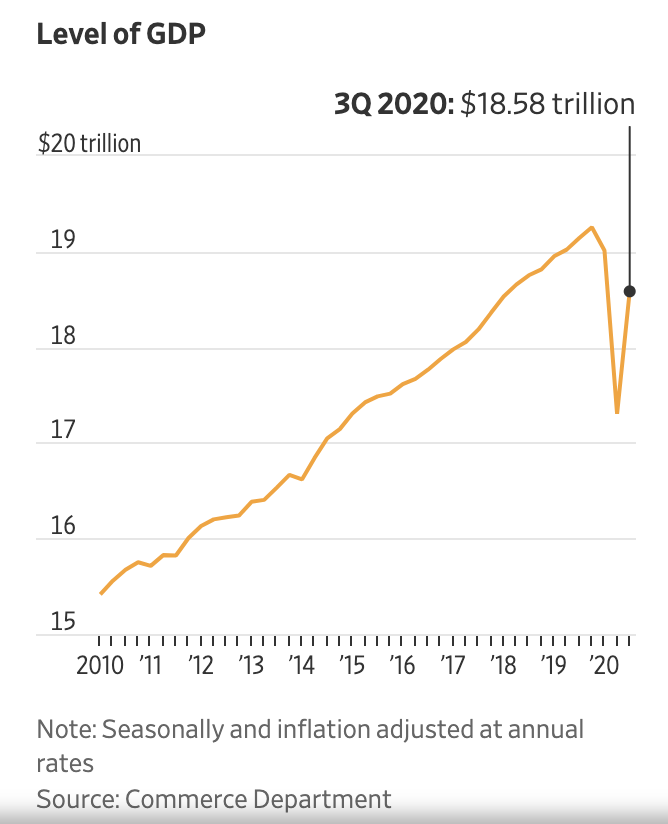

Given the inevitability of the recession as the pandemic and its associated lockdowns continue to ravage the economy for months, Americans wonder “how deep will the damage be and how long will the country take to recover?” Two main factors that help measure the severity of an economic recession are how much real GDP contracts and how much unemployment rises. While the full depth of the recession is still unknown, we expect the health of the economy to decline further as we head into the fourth quarter. According to the Commerce Department, U.S. gross domestic product shrank at an annual rate of 33.0% in the second quarter, an economic shock three times as sharp as the previous record — 10.0% in 1958 — and four times that of the worst quarter during the Great Recession of 2008. More than 40 million people, or roughly one in four Americans, have filed for unemployment benefits since the onset of the coronavirus pandemic in mid-March, an astounding tally that rivals the bleakest years of the Great Depression.

As the U.S. GDP continues to contract, the chances of a quick recovery decline. When the pandemic first began, economists expected a V-shaped recovery, characterized by a sharp economic downturn and a swift rebound. In other words, economists expected the economy to snap back to normal upon the virus being contained and governmental restrictions being lifted, enabling people to return to work and shopping malls, factories to resume, and travels to return to pre-virus levels. However, these predictions were based on the assumption that the outbreak would put a short pause on economic activity that could be reversed. But as lockdowns continue into the third quarter (with disturbances in economic activity to continue for months as any hope of a cure or public vaccine for the virus remains far into the future), a speedy recovery becomes increasingly unlikely.

Although a recession is inevitable, recovery — no matter how fast or slow — is also certain. In fact, a recent report released by the Commerce Department declared that the U.S. GDP grew at a whopping 33.1% annual rate in the third quarter, recovering two-thirds of the ground it lost earlier as coronavirus-related lockdown measures devastated the economy through the first two quarters of the year. However, the recent U.S. surge in infections can hamper further recovery in the fourth quarter as lockdown measures are renewed.

All said and done, in the wake of this pandemic, the grim reality remains that 2020 is on course to be one of the worst years on record for both the U.S. and global economy.

No responses yet